The fatal flaw in EV battery swapping

Battery swapping isn't the future for EVs, but it may be the future for robots

Welcome to Lithium Horizons! This newsletter explores the latest developments, companies, and ideas at the frontiers of energy materials. Subscribe below to get the next article delivered straight to your inbox.

The mainstream narrative positions battery swapping as an improvement over plug-in charging. In this framing, electric vehicle (EV) batteries are treated like propane gas cylinders: arrive, swap a depleted pack for a charged one, and resume driving within minutes (Figure 1).

Proponents present this as a logistics problem. Swapping is faster than charging, and by separating the battery pack from the vehicle's upfront cost it enables a compelling Battery-as-a-Service model. If a third party owns the battery, EV manufacturers simply need to make the physical interface interchangeable

The problem is that a shared physical interface is standardization. Agreeing on pack geometry, connector placement, thermal management interfaces, and structural mounting points requires EV manufacturers to freeze part of their vehicle and battery architecture.

This matters because EV batteries are not interchangeable energy containers. They are highly sensitive, tightly integrated electrochemical systems whose degradation, lifespan, and safety profiles are directly shaped by cell chemistry, thermal history, and pack-level engineering design.

The question, then, is not whether swapping is faster than charging. It is whether a standardized, physically interchangeable battery architecture is compatible with the direction EV technology is evolving.

Increasingly, the answer appears to be no.

The core constraint: standardization under rapid technical change

Battery swapping depends on a strict prerequisite: structural standardization. In practice, this is difficult to achieve in an industry where pack designs are actively diverging.

Different vehicle applications demand different engineering trade-offs (e.g., balancing energy density against power density, or cycle life against fast-charge tolerance), which not only shape the cell design but also pack architecture and integration strategy. Imposing a frozen standard in this environment risks locking out some of the most promising innovations in the field, including cell-to-chassis architectures that treat the battery as a structural component of the vehicle itself.

As a result, EV manufacturers have little incentive to converge on a shared format. The battery pack is the primary lever for differentiation in range, safety, cabin space, and cost. Standardizing the battery means commoditizing the core intellectual property and surrendering product defensibility.

In theory, manufacturers could standardize only the external battery interface while continuing to innovate internally. In practice, however, the battery has become so tightly integrated into vehicle architecture that even partial standardization constrains engineering freedom. The economic cost of adopting a common format therefore remains high.

Industry-wide standardization is, for these reasons, a non-starter in the near to medium term.

What about China?

The most cited counterexample is China, where NIO has built over 3,000 swap stations across 700 cities. On the surface, this looks like evidence that battery swapping can scale.

But if one looks closer, it shows that NIO’s network has historically worked because it was a closed ecosystem: one company, one proprietary system. While they are currently trying to open their platform to partners like Changan and others, achieving true cross-brand physical standardization remains, as a CATL executive recently noted, ‘‘the most important issue we still need to solve.’’

NIO demonstrates that battery swapping can scale operationally. The unresolved question is whether such systems can scale profitably while expanding beyond a tightly controlled ecosystem. The fact that standardization remains an open challenge after a decade of deployment suggests that the difficulty is not temporary.

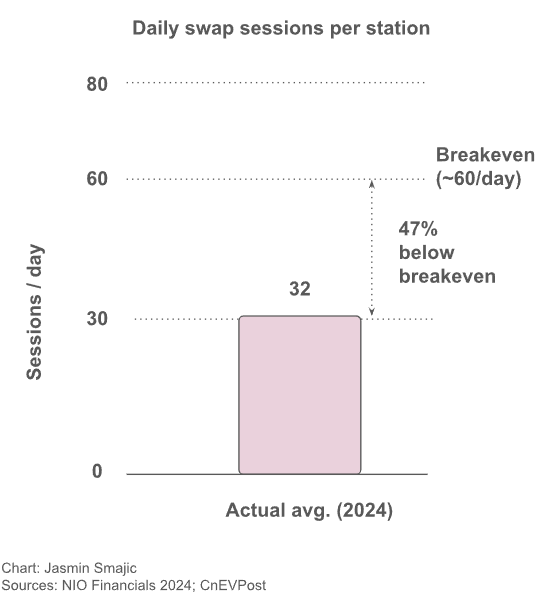

The economics reinforce this. NIO’s swap business lost €400 million (3.12 billion yuan) in 2024 alone, with stations averaging just 32 service sessions per day (Figure 2).

Therefore, China demonstrates that battery swapping can function within a tightly controlled and vertically integrated environment. It says nothing about whether swapping can go mainstream in an open, competitive market.

The hidden cost: battery inventory

Swapping infrastructure requires more than stations. It also requires spare batteries. Every swap location must maintain an inventory of charged packs capable of handling demand spikes. Unlike charging infrastructure, where the battery remains inside the vehicle, swapping infrastructure concentrates large amounts of capital in batteries that spend much of their time waiting for use.

This creates another economic hurdle. The swap station operator is not only financing land, robotics, maintenance, and grid connections, but also a pool of idle battery assets. Any assessment of battery swapping economics must therefore account for both infrastructure costs and battery inventory costs.

This inventory burden is largely absent from discussions that compare swapping and charging solely on replenishment speed.

Charging has narrowed the gap

Modern EV charging has improved substantially over the past decade. Higher-voltage architecture operating around 800 V has lowered currents needed to transfer power while reducing heat generation. Cell-level thermal management now allows for aggressive, highly optimized charging curves. And larger battery packs have reduced the frequency of charging events altogether.1

For most consumers, a 20-minute charging stop is enough to add meaningful highway range.2 The marginal benefit of reducing that stop to a three-minute battery swap is simply not large enough to justify the infrastructure and logistical complexity of swapping networks.

Nor is it necessary. Most charging occurs while vehicles are already parked: overnight at home, during working hours, or at destination locations. In those cases, reducing charging time from several hours to a few minutes creates little additional value because the vehicle was not needed during that period anyway.

This conclusion, however, may obscure a more important point: battery swapping may not be a consumer mobility solution at all.

The one segment where swapping makes sense

A passenger vehicle is idle most of the time. A commercial vehicle is an economic asset whose utilization directly dictates the total cost of ownership and fleet profitability. Under commercial operating conditions, charging time is a revenue-generating capacity sitting unused.

Consider a municipal city bus fleet operating on fixed, predictable routes. Each bus returns to a centralized depot to replenish its energy. A typical 150 kWh bus battery charged via a standard 50 kW depot DC charger requires several hours to fully recharge. At fleet scale, this creates compounding idle time (Figure 3).

The intuitive response is to upgrade to high-power charging.3 But this approach runs into real constraints: power grid saturation, permitting timelines, and the cost of transformer upgrades (particularly in older, diesel-era depots not designed for high electrical loads).

Here, battery swapping offers a possible alternative. Instead of fast-charging the vehicles, the fleet operator maintains a pool of identical batteries at the depot. These packs are charged slowly and efficiently during off-peak hours, considerably flattening the depot's peak electrical demand. When a bus rolls in, an automated system swaps the pack in minutes.

In this case, the bottleneck shifts from vehicle downtime to inventory management. Whether the resulting utilization gains are sufficient to justify the added inventory costs becomes a fleet-specific economic question.

Second-order constraint: the human factor

Even within commercial fleets, optimizing vehicle downtime through battery swapping ignores a critical operational variable: the human driver.

Most countries enforce mandatory rest periods for commercial fleet drivers. Under EU labor frameworks, for example, a truck driver must take a 45-minute break after every 4.5 hours of driving. When a vehicle is legally required to sit idle while its operator rests, the economic value of a three-minute battery swap evaporates.

A high-power fast charger, such as the Megawatt Charging System (MCS), can easily replenish the pack during that mandatory human rest cycle, with no swapping infrastructure required.4 Any economic case for swapping must therefore remain compelling against a moving technological target rather than today's charging capabilities.

Swapping only yields a positive return on investment when the energy replenishment cycle cannot be absorbed into existing operational schedules. Which brings us to the one context where that condition is satisfied.

Removing the human factor

The strongest case for battery swapping emerges when the human driver is removed from the equation entirely. Picture a Waymo sitting at a charger at 4pm, no passengers, no driver, no reason to be parked except that its battery is at 10% state of charge (SOC).

In fully autonomous operating environments, such as urban robotaxi networks, automated port logistics, warehouse fleets, vehicles are no longer bound by labor laws or biological rest cycles. Asset utilization approaches 24/7, constrained only by maintenance windows and energy replenishment. Waymo’s robotaxis are already designed around this model: continuous operation, with downtime as the enemy of unit economics (Figure 4).

Consider what this means at scale. A fleet of 10,000 autonomous vehicles loses 10,000 vehicle-hours daily to charging. Swapping recovers 8,300 of them.5

Baidu's sixth-generation robotaxi, operating commercially in Wuhan, runs on a battery-swapping architecture in which vehicles autonomously schedule their own swaps based on real-time battery level and station availability. The human has been removed not just from the driving seat, but from the energy management loop entirely.

Crucially, this context satisfies all conditions that make swapping viable: a centralized operator, a standardized vehicle platform, predictable routes, and continuous utilization. The standardization problem that is intractable across a fragmented consumer market becomes solvable when a single fleet operator controls both the vehicle specification and the infrastructure.

Battery swapping's future, if it has one in passenger-adjacent mobility, will most likely be written by autonomous fleet operators.6

Conclusion

Battery swapping is often framed as a faster version of charging. This misses the central issue. The debate is not fundamentally about energy replenishment speed but about asset utilization. In environments where vehicles spend most of their lives parked, charging remains the simpler solution. In environments where every minute of downtime carries an economic cost, swapping becomes increasingly attractive.

It is a niche infrastructure model whose viability depends entirely on system-level conditions: standardization, asset utilization, grid constraints, and labor economics.

For passenger EVs, fast charging has likely established itself as the optimal solution for long routes. For commercial fleets with human drivers, the case remains conditional. And for autonomous systems operating at scale, battery swapping may yet prove to be critical infrastructure; not because it is faster than charging, but because it is the only recharge model that does not require the asset to stop earning.

The future of battery swapping may therefore depend less on batteries themselves than on who owns the vehicles. As long as cars remain personal possessions, charging is likely to dominate. If transportation becomes increasingly autonomous and fleet-based, battery swapping could evolve from a niche solution into critical infrastructure.

That’s all for now — until next time! 🔋

If you enjoyed reading this piece, consider sharing and subscribing to Lithium Horizons. It helps support future articles on materials powering the energy transition.

In 2025, the weighted average EV battery size remained stable in the EU and China, at close to 70 kWh and 60 kWh, respectively. In the United States, battery sizes reached 90 kWh.

A 20-minute stop on a 150 kW charger will deliver around 40 kWh of energy. For an average EV, that translates to 200 to 250 km of added range.

One way to avoid this pain is to consider charging power expansion from the beginning. The depot can be designed from the beginning to accommodate future upgrades. The issue is, however, in the fact that many of these depots are old and diesel-based, so transitioning to an electric fleet is unavoidably complicated.

MCS can deliver powers north of 1 MW, allowing a Class 8 truck to charge from 20% to 80% in 30-45 minutes. And while this approach requires costly grid interconnection upgrades, corridor charging locations can sometimes leverage existing high-voltage transmission lines near major freight highways, whereas urban depots face dense spatial constraints.

Assuming a fleet of 10,000 autonomous vehicles operating continuously, each requiring two 30-minute charging stops per 24-hour cycle: total daily charging downtime is 10,000 vehicle-hours (10,000 × 2 × 0.5 hours). Replacing those stops with 5-minute swaps reduces daily downtime and recovers 8,300 vehicle-hours of productive capacity. At an illustrative revenue rate of 20 EUR per vehicle-hour, that represents 166,000 EUR in recovered earning potential daily across the fleet.

One may ask: if batteries can be charged in 5 minutes, doesn’t that eliminate the swapping advantage across all EV sectors? Fast charging battery cells are optimized for high power acceptance, not cycle longevity; they are also more expensive. These are not the cells one would use for cost-sensitive deployments that require long cycle life, such as warehouse logistics or port automation.