Is the lithium market finally rebalancing?

Beijing’s withdrawal of export rebates and the mining consolidation signal a transition from volume to value-driven growth

Welcome to Lithium Horizons! This newsletter explores the latest developments, companies, and ideas at the frontiers of energy materials. Subscribe below to get the next article delivered straight to your inbox.

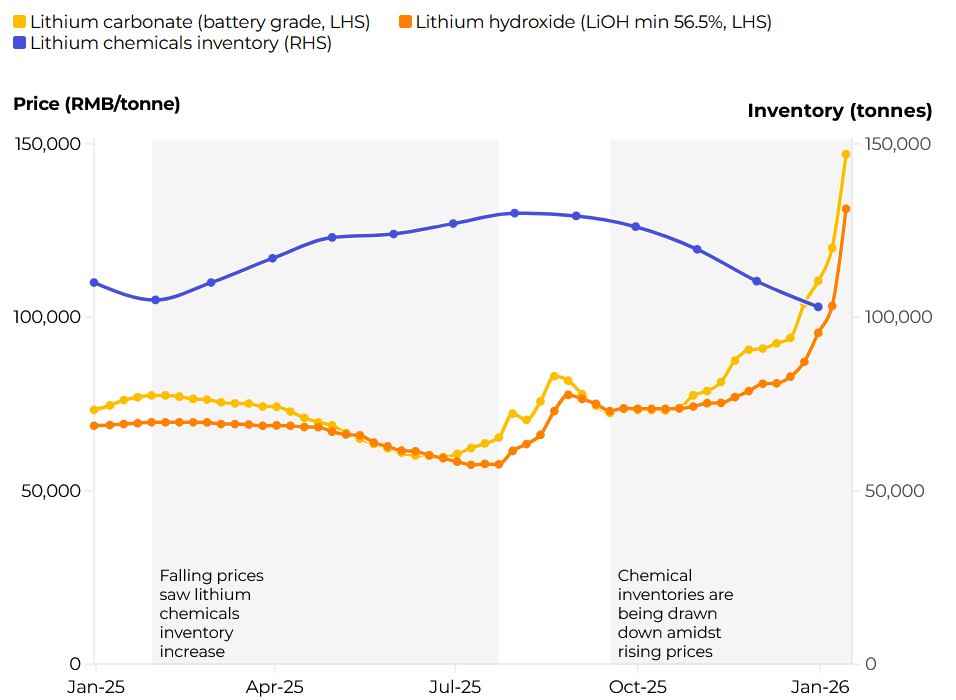

For much of the past two years, the battery industry has endured a ‘‘lithium winter’’. After the mania of 2022 saw prices peak at over €70,000 per ton, the market faced a steep correction amid inventory overhangs, slowing (though still positive) EV growth, and a flood of new lepidolite capacity in China that crushed the spot market. By mid-2025, lithium carbonate bottomed out near €10,000–€12,000 per ton, forcing high-cost miners to pause projects.

That cycle may now be turning, not because demand suddenly surged, but because Beijing has decided that deflation has gone far enough. On January 9, 2026, it issued Announcement No. 2, slashing VAT export rebates from 9% to 6%, effective April 1, with a total phase-out by January 1, 2027. This represents a massive hit to profitability. In an industry where net margins for second-tier exporters often hover around 5%, a 3% cut is enough to decide a company’s fate.1

Before that, in December 2025, China tightened the regulatory oversight of lithium mines and cancelled 27 mining licenses in Yichun, Jiangxi. While the number sounds alarming, the reality is that this move was more of a ‘‘clean-up’’ and consolidation operation. Most of these permits were inactive and many of the mines operated under “ceramic clay” or “limestone” permits to bypass the stricter oversight required for strategic minerals, such as lithium. Beijing is effectively closing these loopholes and forcing a transition from disorderly expansion to industrial discipline.

These policies triggered a rapid response across the market, with buyers accelerating purchases and inventory levels dropping ahead of implementation deadlines. In just the first six weeks of 2026, prices have rallied roughly 30%, currently stabilizing near €18,000 per ton (Figure 1).

Taken together, these developments suggest that China is placing a structural floor under lithium pricing; we have likely seen the lowest levels of this cycle.