Is the lithium market finally rebalancing?

Beijing’s withdrawal of export rebates and the mining consolidation signal a transition from volume to value-driven growth

Welcome to Lithium Horizons! This newsletter explores the latest developments, companies, and ideas at the frontiers of energy materials. Subscribe below to get the next article delivered straight to your inbox.

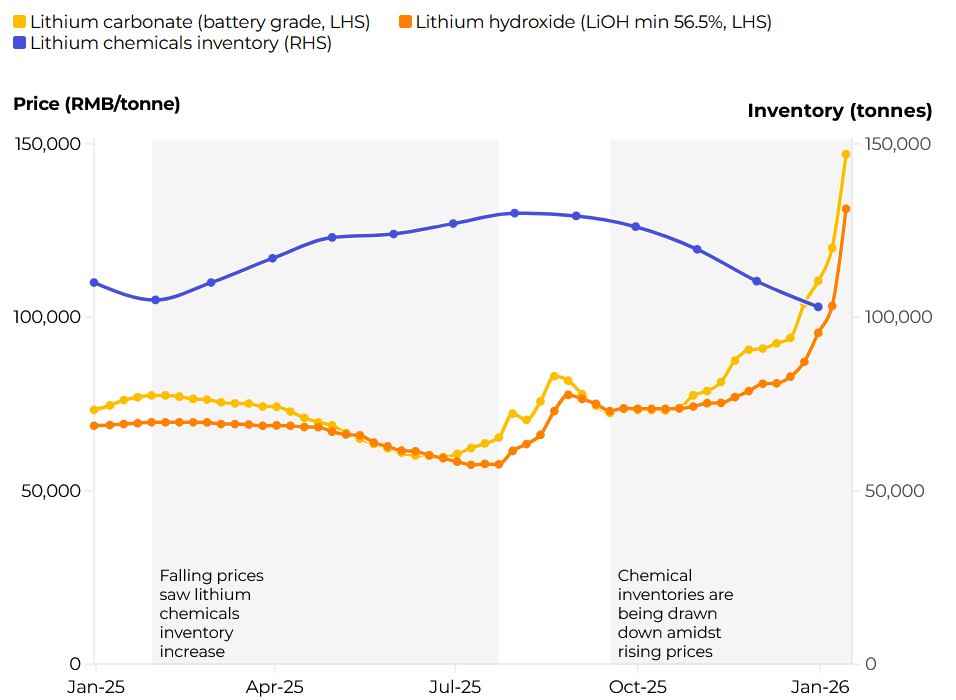

For much of the past two years, the battery industry has endured a ‘‘lithium winter’’. After the mania of 2022 saw prices peak at over €70,000 per ton, the market faced a steep correction amid inventory overhangs, slowing (though still positive) EV growth, and a flood of new lepidolite capacity in China that crushed the spot market. By mid-2025, lithium carbonate bottomed out near €10,000–€12,000 per ton, forcing high-cost miners to pause projects.

That cycle may now be turning, not because demand suddenly surged, but because Beijing has decided that deflation has gone far enough. On January 9, 2026, it issued Announcement No. 2, slashing VAT export rebates from 9% to 6%, effective April 1, with a total phase-out by January 1, 2027. This represents a massive hit to profitability. In an industry where net margins for second-tier exporters often hover around 5%, a 3% cut is enough to decide a company’s fate.1

Before that, in December 2025, China tightened the regulatory oversight of lithium mines and cancelled 27 mining licenses in Yichun, Jiangxi. While the number sounds alarming, the reality is that this move was more of a ‘‘clean-up’’ and consolidation operation. Most of these permits were inactive and many of the mines operated under “ceramic clay” or “limestone” permits to bypass the stricter oversight required for strategic minerals, such as lithium. Beijing is effectively closing these loopholes and forcing a transition from disorderly expansion to industrial discipline.

These policies triggered a rapid response across the market, with buyers accelerating purchases and inventory levels dropping ahead of implementation deadlines. In just the first six weeks of 2026, prices have rallied roughly 30%, currently stabilizing near €18,000 per ton (Figure 1).

Taken together, these developments suggest that China is placing a structural floor under lithium pricing; we have likely seen the lowest levels of this cycle.

Combating the race to the bottom

Why would the world’s battery hegemon intentionally make its own exports more expensive? The answer lies in a single word, Neijuan (内卷), which describes a destructive internal competition that erodes margins and undermines industrial sustainability. It has been visible in Chinese solar, EV manufacturing, and battery technology (Figure 2).

For years, intense competition among lithium processors and battery manufacturers drove prices down to levels that compressed profitability across the ecosystem. Subsidies and VAT rebates amplified this race to the bottom by enabling exports at razor-thin margins — a deliberate strategy to allow Chinese companies to compete in global markets through low prices and high volumes.

In 2026, however, this strategy is no longer suitable. China is shifting from a volume-driven export model to a value-driven one.

By cancelling old mining permits and stripping away export tax breaks, it is trying to stabilize lithium prices and push the industry to consolidate. Beijing is restoring fiscal discipline, forcing inefficient producers who only survived on rebates out of the market, and recapturing billions in tax revenues.

Furthermore, now that national champions and globally competitive firms are established, perpetual subsidy-fueled undercutting ceases to serve a strategic purpose. This is in line with the Chinese approach in adjacent sectors, such as graphite and battery cell technology.

However, there is also a strategic external dimension. By voluntarily reducing export rebates, China is effectively disarming the EU and US anti-dumping investigators who have intensified scrutiny of Chinese battery pricing, with anti-dumping investigations and proposals to blacklist firms accused of undercutting. In doing so, Beijing may be trying to preserve global market access at a time when protectionist tendencies are rising.

In 2022, China used pricing power to expand global share. In 2026, it is using discipline to protect profitability.

Upward price pressure

With rebate phase-out on the horizon, exporters are incentivized to front-load shipments, while buyers are incentivized to stockpile. This dynamic alone has contributed to recent pricing momentum in lithium compounds.

The lithium market is unlikely to revisit the speculative extremes of 2022. Price is expected to continue increasing in the near term, which may pressure battery giants to restart mining operations, as they become profitable once more.

Now that a more disciplined approach to lithium production and processing is expected, inefficient producers are forced out. This also means that the technical know-how and innovation that enables cost-savings will be the real moat. Furthermore, it means that the price gap between Chinese and burgeoning Western production will narrow, potentially creating strong long-term pressure toward the localization of supply chains.

The ‘‘lithium winter’’ was not a failure of demand. It was a correction of excess supply discipline. Beijing’s latest move suggests that the era of uncontrolled expansion is over and the era of margin discipline has begun.

That’s all for now — until next time! 🔋

If you enjoyed reading this piece, consider sharing or subscribing to Lithium Horizons. It helps support future articles on materials powering the energy transition.

At current lithium carbonate prices of roughly €18,000 per ton, a 3% rebate is approximately €540 per ton in lost margin. For exporters operating with net margins in the 5% range (€900–€1,200 per ton), this represents a 35–50% compression in profitability.