The quiet crisis of graphite

Why graphite is the bottleneck in the battery trade war

Welcome to Lithium Horizons! This newsletter explores the latest developments, companies, and ideas at the frontiers of energy materials. Subscribe below to get the next article delivered straight to your inbox.

In late 2023, the global energy market was shaken when China, which is responsible for refining more than 90% of the world’s graphite into battery-grade anodes, announced export controls on the mineral. While the world has been obsessing over lithium, a quieter and arguably more dangerous crisis was unfolding.

The West has poured hundreds of billions of dollars into electric vehicles and battery gigafactories. Yet it remains almost entirely dependent on a single country for one material that no lithium-ion battery can function without: graphite.

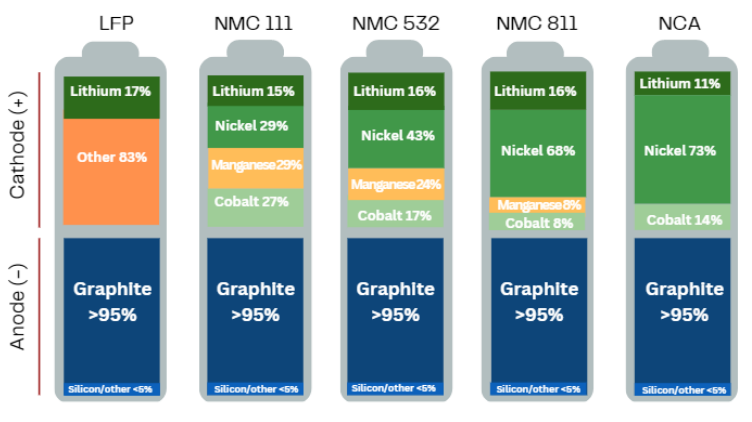

Often overshadowed by its flashier peers (e.g., lithium and nickel), graphite is the workhorse of the battery industry. Every lithium-ion battery, from smartphones to grid-scale energy storage, relies on graphite as the dominant anode material.1 Roughly 95% of the anode material in today’s batteries is graphite and, by weight, a battery cell contains up to ten times more graphite than lithium (Figure 1). Without graphite, lithium-ion batteries simply would not work.

And batteries are only part of the story. Around 40% of global graphite consumption goes into steelmaking. It is also used in high-temperature crucibles, dry lubricants, conductive brushes for electric motors, rocket nozzles, heat shields, and, most famously, pencils. From the furnaces of the steel age to the batteries of the electric age, graphite has remained indispensable.

Geopolitical considerations

Graphite’s supply chain is far more concentrated than lithium’s, creating a strategic vulnerability that is only now being fully appreciated.

Today, China controls nearly every critical link:

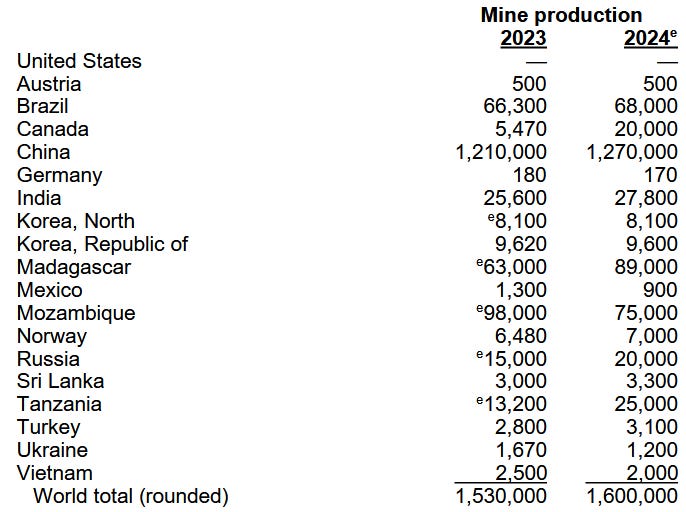

>70% of global natural graphite mining (Figure 2)

~95% of the synthetic graphite production

>90% of battery-grade anode processing

This concentration gives China immense geopolitical leverage. In late 2023, Beijing introduced permit requirements for certain graphite exports. In October 2025, these measures escalated with Announcement No. 58, targeting not just material exports, but also the specialized furnaces, equipment, and technical know-how required to manufacture high-performance anodes.2

Although these restrictions were temporarily suspended in December 2025, the suspension expires in November 2026. The West now has less than a year to build meaningful domestic capacity before the supply is once again constrained.

It raises an uncomfortable question: what if the energy transition isn’t limited by lithium, but by the same material found in your pencil?

In this article, we examine:

Why graphite is indispensable to lithium-ion batteries

The processing technologies China is protecting

Graphite projects emerging outside of China

Potential alternatives that could weaken the graphite monopoly

Let’s dive in! 🔋